The report discusses Poland’s status as a developed country benefiting from European Union membership but acknowledges a significant gap compared to leading European economies. Emphasizing the importance of supporting domestic potential for economic independence, the authors cite disruptions in supply chains due to the COVID-19 pandemic and the impact of the Russia-Ukraine conflict. Drawing inspiration from Estonia’s success in innovation, particularly in technology with companies like Bolt and Skype, the report stresses the need for Poland to prioritize technological advancements for economic resilience. The startup sector is identified as a crucial player in fostering innovation, but financial support is deemed essential from both the state and private investors. The challenges faced by Polish startups are highlighted, including the negative effects of the global economic crisis.

10 Main Takeaways:

- One-third of Polish startups prioritize keywords like AI, deeptech, and IoT in their core products or services.

- While men dominate the majority of startup employees, 8% of companies have 76-100% women, with the highest percentage in cyber security startups.

- Mazovia and Lower Silesia are the most active regions for startups, with other regions like Lesser Poland and Pomerania also showing significant presence.

- More than half of startups (51%) report better revenue than the previous year, with 26% slightly better, and 8% unchanged.

- Domestic VC funds (25%) are the primary source of external funding, followed by foreign VC funds (8%) and domestic business angels (24%).

- Industry portals are the main source of legal change knowledge (65%), followed by social media (47%), press and TV (37%), official EU websites (34%), and Startup Poland Foundation’s website (20%).

- 42% find legal changes problematic due to interpretation challenges, 41% are unsure which changes affect them, and 31% struggle to keep up with frequent changes.

- The cost of hiring employees is the primary barrier to startup development (54%), followed by funding acquisition (49%), bureaucratic challenges (37%), and the perceived length and cost of the startup process (4%).

- Startups seek support in funding (69%), cooperation with investors (48%), company management (31%), team management (23%), legal compliance (28%), and cybersecurity (18%).

- Startups commonly complain about the lack of feedback from investors (45%), exploitation of founder’s ignorance (44%), and overly aggressive investor policies (42%).

Polish Startup – Profile

The Polish startup market is predominantly composed of very young companies, consistent with the common startup characteristics of a short operational period, a focus on rapid growth, and a high risk of failure. Various analyses, including those by Failory, indicate a high failure rate, with 9 out of 10 startups failing, and 20% going out of business within a year. The survey conducted by the Startup Poland Foundation reveals that nearly one in four respondents have been in business for less than a year, 28% for one to two years, and the highest percentage between three and four years. Companies operating for more than five years constitute 15%, with those operating for more than 10 years excluded due to the startup definition. This survey provides a representative cross-section of the Polish startup community, offering insights into their current situations, needs, and concerns.

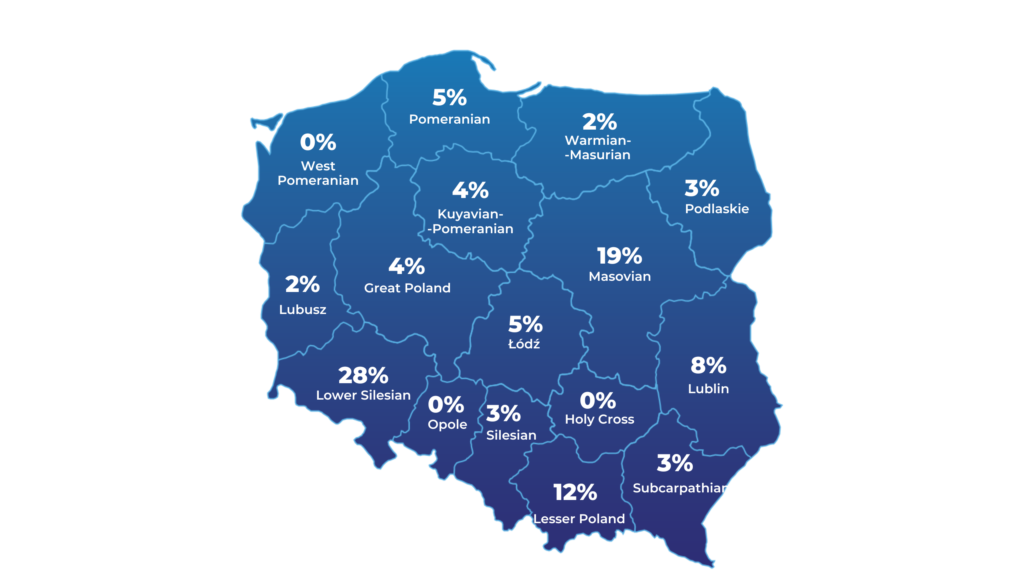

The map of Polish startups shows consistent rankings, with the Lower Silesian region sharing the title of ‘Polish Silicon Valley’ with the Masovian region, primarily Warsaw. Lower Silesia’s economic strength, historical factors, a robust academic and scientific community, and better infrastructure contribute to its consistent success in startup rankings. The region’s favorable geographical location, particularly its proximity to the German border, allows many companies to engage with German industries, fostering innovation and technology development by local startups. While the survey reveals that Lower Silesia and Masovia lead in creating startups, the study also explores regions where startups are operational. In terms of startup creation, Lower Silesia dominates with 28%, followed by Masovia at 19%, while Lesser Poland is on the podium but with a lower percentage (12%).

The weakest regions in Poland in terms of startups continue to be the smallest voivodeships, including the Lubusz Voivodeship (2%), the Holy Cross Voivodeship, and the Opole Voivodeship (1% each).

Specialization of the Polish startups

Polish startups specialize significantly in Artificial Intelligence (AI), with one-third of surveyed startups (33%) considering AI, deeptech, and IoT (Internet of Things) as keywords reflecting the nature of their primary product or service. The emergence of ChatGPT by OpenAI has been recognized as a technological game-changer, prompting global giants to work on competing solutions. Although the Polish technology sector may not compete on an equal footing with global giants, the country boasts highly regarded programmers who contribute to the development of tools based on advanced algorithms. Some Polish startups, like SentiOne, have already created proprietary conversational AI technology for customer service automation. Despite the potential, the survey suggests that AI is a keyword prominently indicated by Polish startups, but the country may face challenges in funding such advanced technologies compared to global markets.

Foodtech and cleantech

The report highlights the significance of foodtech and cleantech industries in promoting economic resilience and sustainable practices in Poland. It emphasizes the challenges posed by population growth, climate change, and environmental issues linked to industrial food production. The implementation of new technologies, especially in agriculture (referred to as agriculture 4.0), is seen as crucial for addressing these challenges. The COVID-19 pandemic distorted growth figures for the foodtech industry, with a surge in investments during the pandemic period followed by a decline in investor interest in 2022.

Funding for innovation in agrifood businesses is available through EU and national funds, and startups in the agritech and foodtech sectors play a crucial role in contributing to the agro-technological revolution. Despite the pandemic-related challenges, the Startup Poland Foundation’s surveys indicate a rising trend in startups focusing on agritech and foodtech, reaching 5% and 8% respectively in the latest survey. The text emphasizes the importance of national funding for research and development in these areas to ensure continued growth and resilience in the food production sector. Additionally, the skillful use of technology in agriculture is viewed as essential for Poland’s economic resilience and the promotion of a sustainable economy. Startups like Proterinrise, HiProMine, Foodsi, and Miesna Paczka are highlighted as examples of domestic companies contributing to these goals, as recognized by the Polish Development Fund.

The cleantech segment is becoming increasingly important in the startup market, with 7% of surveyed startups in the Startup Poland Foundation’s survey identifying as cleantech/greentech. The foundation’s report ‘Technology for Energy’ in 2022 focused on the ESG revolution, emphasizing the need for technologies reducing greenhouse gas emissions and supporting renewable energy. However, the report highlighted challenges, including restrictions on wind power plants and issues with the cost-effectiveness of photovoltaics. The cleantech sector faces systemic problems like outdated infrastructure and the lack of efficient energy storage. Despite VC investment growth in European cleantech, the Polish cleantech sector is not among the global or European leaders. The energy crisis caused by Russia’s invasion of Ukraine underscored the importance of energy independence, but Poland has not fully exploited this opportunity. The success of innovative solutions in the Polish energy sector depends on legal changes and a shift in mentality among decision-makers and investors. Cleantech founders believe changes are inevitable, and failure to keep up with global trends in this area will be increasingly costly for any national economy.

Medtech

Startups in the medical sector, known as medtechs, enjoy a good reputation among investors due to the broad relevance of medical care and the ongoing progress in supporting technologies. The medtech industry has experienced significant growth, reaching a value of approximately USD 19.4 billion, with an expected increase to USD 23.2 billion by 2028. However, global medtech capital inflows have slowed down, with a decline in investor activity in the first quarter of the year, followed by a slight rebound in the second quarter.

Despite the positive outlook, the medtech industry faces challenges such as a complex regulatory environment, diverse funding sources, clinical trial requirements, recruiting high-caliber professionals, and intense competition. Innovations in medicine are costly and time-consuming, impacting the quick return on investments. In Poland, 17% of surveyed startups identified as medtech, indicating an increase from previous years.

The Top Disruptors in Healthcare report highlighted the primary challenge for medical startups in Poland as the difficulty of finding investors and funding, mentioned by 44% of medtechs. Funding sources for Polish medtechs include founders’ own funds (56%), private investors (41%), European fund grants (40%), Polish VC funds (33%), and foreign funds (13%).